Skip to main content

Go to main navigation

Go to language selector

Search

Free text

Free text

Search

Swedish Match

Menu

Close

Our websites

svenska

Search

Search

Close

Close

Swedish Match websites

Image Bank

Swedish Match Brasil

Swedish Match Industries

Snus and Match Museum

Brand websites

Smokefree

Swedish Match e-commerce service (SE)

General (US)

Longhorn (US)

Pinkerton Tobacco

ZYN (SE)

Lights

Cricket

Nitedals

Redheads

Other

Swedish Match Denmark

Swedish Match Norway

The Solstickan Foundation (SE)

Home

Our company

More

Less

Our company

About us

Markets

More

Less

Our product categories and markets

Company history

More

Less

Svenska Tobaks AB

Svenska Tändsticks AB

Swedish Match AB

Corporate Governance

More

Less

Articles of association

AGM minutes

Our business

More

Less

Our business

Smokefree

More

Less

Nicotine products and regulations

History of snus

Snus production

Cigars

More

Less

History of cigars

Lights

Sustainability

More

Less

Sustainability

Strategy and approach

Materiality assessment

More

Less

Sustainable Tobacco Program

Code of Conduct

More

Less

Supplier Code of Conduct

Swedish Match North America Terms and Conditions

Sustainability information

More

Less

Environment

Compliance

Employees and social conditions

Human rights

Sustainability reporting

Investors

More

Less

Investors

Share holdings

Financial reports

Debt information

More

Less

Debt programs

Outstanding bonds

Media

More

Less

Media

Press releases and news

Swedish Match logotype

Images

Videos

Swedish Match Norway

More

Less

Our history

Sustainability

Media contacts

Snus and health

More

Less

Snus and health

Our standpoint

Swedish Match Scientific Publications

More

Less

Our Scientific Publications

GOTHIATEK

®

More

Less

GOTHIATEK

®

standard

The Swedish Experience

Research on snus

Smoking cessation

Snus and the Swedish Food Act

Nicotine

More

Less

Nicotine labeling of Swedish Match products

Snus, nicotine and nicotine addiction

Tobacco use

More

Less

Tobacco use in figures

Career

More

Less

Career

Employee strategy

Our culture

Work environment

Diversity and non-discrimination

Competence development

Compensation and benefits

Vacant positions

Student

Search

Our websites

Language:

English

svenska

Investors

Share holdings

Financial reports

Debt information

Financial reports

2024

Annual report 2024

Mar 25, 2025 8:09 AM CET

Annual report 2024

2023

Annual report 2023

Jun 28, 2024 12:39 PM CET

Annual report 2023

2022

Annual report 2022

Apr 28, 2023 1:35 PM CET

Annual report 2022

Interim reports 2022

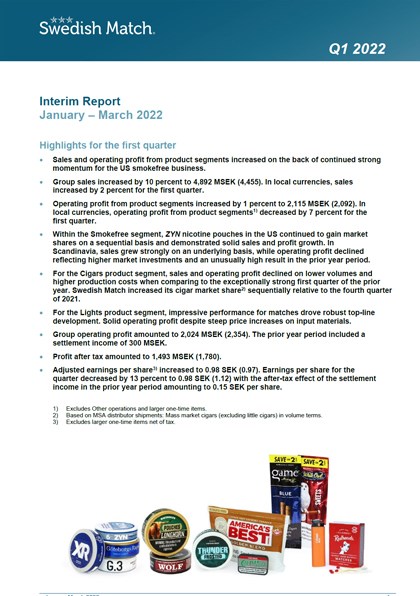

Q1

May 11, 2022 6:15 AM CET

Report

Q2

Jul 22, 2022 6:15 AM CET

Report

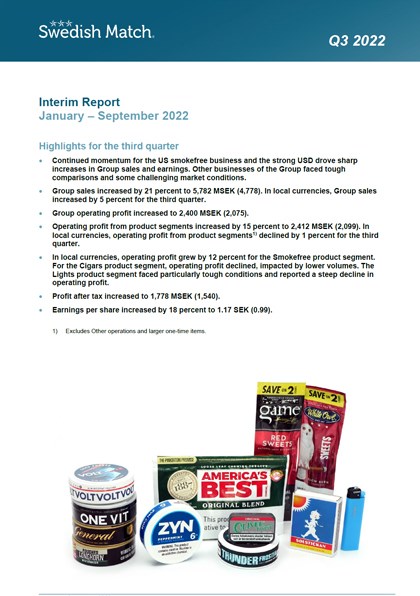

Q3

Oct 28, 2022 6:15 AM CET

Report

2021

Annual report 2021

Mar 25, 2022 10:00 AM CET

Overview page 2021

Annual report 2021

Annual report 2021 (ESEF)

Annual report 2021 XBRL viewer

Interim reports 2021

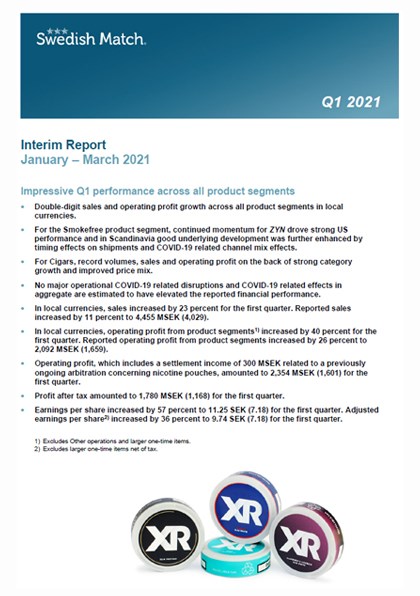

Q1

Apr 30, 2021 6:15 AM CET

Report

Q2

Jul 20, 2021 6:15 AM CET

Report

Q3

Oct 27, 2021 6:15 AM CET

Report

Q4

Feb 16, 2022 7:15 AM CET

Report

2020

Annual report 2020

Mar 16, 2021 2:00 PM CET

Overview page 2020

Annual report 2020

Interim reports 2020

Q1

Apr 27, 2020 6:15 AM CET

Report

Q2

Jul 17, 2020 6:15 AM CET

Report

Q3

Oct 27, 2020 7:15 AM CET

Report

Q4

Feb 10, 2021 7:15 AM CET

Report

2019

Annual report 2019

Mar 6, 2020 1:03 PM CET

Overview page 2019

Annual report 2019

Interim reports 2019

Q1

May 9, 2019 6:15 AM CET

Report

Q2

Jul 18, 2019 6:15 AM CET

Report

Q3

Oct 25, 2019 6:15 AM CET

Report

Q4

Feb 12, 2020 7:15 AM CET

Report

2018

Annual report 2018

Mar 18, 2019 10:00 AM CET

Overview page 2018

Annual report 2018

Interim reports 2018

Q1

May 4, 2018 6:15 AM CET

Report

Q2

Jul 19, 2018 6:15 AM CET

Report

Q3

Oct 26, 2018 6:15 AM CET

Report

Q4

Feb 13, 2019 7:15 AM CET

Report

2017

Annual report 2017

Mar 19, 2018 2:30 PM CET

Overview page 2017

Annual report 2017

Interim reports 2017

Q1

May 8, 2017 6:15 AM CET

Report

Q2

Jul 21, 2017 6:15 AM CET

Report

Q3

Oct 27, 2017 6:15 AM CET

Report

Q4

Feb 14, 2018 7:15 AM CET

Report

2016

Annual report 2016

Mar 24, 2017 10:30 AM CET

Annual report 2016

Interim reports 2016

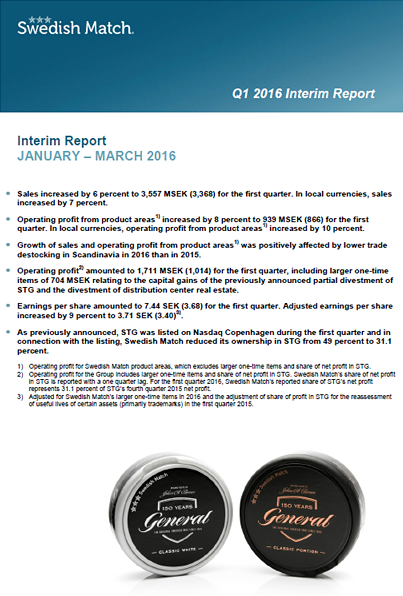

Q1

May 4, 2016 6:15 AM CET

Report

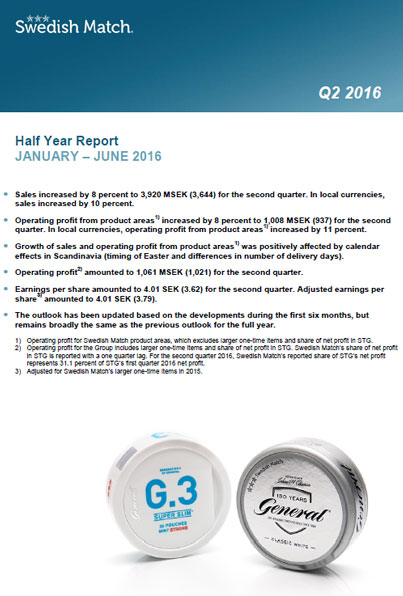

Q2

Jul 22, 2016 6:15 AM CET

Report

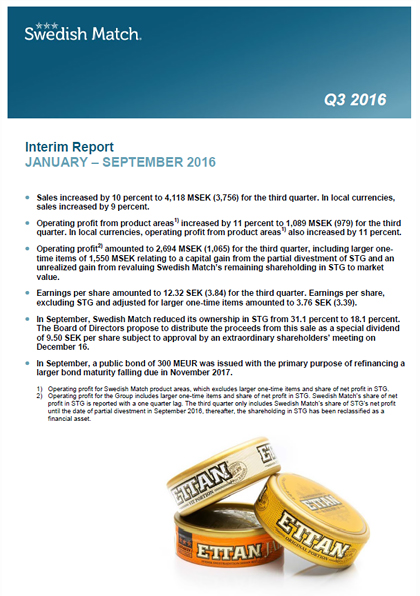

Q3

Oct 28, 2016 6:15 AM CET

Report

Q4

Feb 17, 2017 7:15 AM CET

Report

2015

Annual report 2015

Mar 24, 2016 9:30 AM CET

Annual report 2015

Interim reports 2015

Q1

May 8, 2015 6:15 AM CET

Report

Q2

Jul 17, 2015 6:15 AM CET

Report

Q3

Nov 4, 2015 7:15 AM CET

Report

Q4

Feb 19, 2016 7:15 AM CET

Report

2014

Annual report 2014

Mar 20, 2015 2:00 PM CET

Annual report 2014

Interim reports 2014

Q1

May 9, 2014 6:15 AM CET

Report

Q2

Jul 18, 2014 6:15 AM CET

Report

Q3

Oct 24, 2014 6:15 AM CET

Report

Q4

Feb 18, 2015 7:15 AM CET

Report

2013

Annual report 2013

Mar 25, 2014 1:31 PM CET

Annual report 2013

Interim reports 2013

Q1

Apr 29, 2013 6:15 AM CET

Report

Q2

Jul 19, 2013 6:15 AM CET

Report

Q3

Oct 29, 2013 7:15 AM CET

Report

Q4

Feb 19, 2014 7:15 AM CET

Report

2012

Annual report 2012

Mar 25, 2013 3:00 PM CET

Annual Report 2012

Interim reports 2012

Q1

May 4, 2012 6:15 AM CET

Report

Q2

Jul 20, 2012 6:15 AM CET

Report

Q3

Oct 30, 2012 7:15 AM CET

Report

Q4

Feb 20, 2013 7:15 AM CET

Report

2011

Annual report 2011

Mar 30, 2012 11:00 AM CET

Annual Report 2011

Interim reports 2011

Q1

May 4, 2011 6:00 AM CET

Report

Q2

Jul 20, 2011 6:00 AM CET

Report

Q3

Oct 26, 2011 6:01 AM CET

Report

Q4

Feb 22, 2012 7:16 AM CET

Report

2010

Annual report 2010

Apr 4, 2011 7:57 AM CET

Annual report 2010

Interim reports 2010

Q1

Apr 29, 2010 6:01 AM CET

Report

Q2

Jul 21, 2010 6:00 AM CET

Report

Q3

Oct 27, 2010 6:01 AM CET

Report

Q4

Feb 23, 2011 7:01 AM CET

Report

2009

Annual report 2009

Mar 31, 2010 1:26 PM CET

Annual report 2009

Interim reports 2009

Q1

Apr 30, 2009 6:02 AM CET

Report

Q2

Jul 17, 2009 6:01 AM CET

Report

Q3

Oct 27, 2009 7:00 AM CET

Report

Q4

Feb 25, 2010 7:01 AM CET

Report

2008

Annual report 2008

Apr 1, 2009 9:18 AM CET

Annual report 2008

Interim reports 2008

Q1

Apr 25, 2008 9:49 AM CET

Report

Q2

Jul 18, 2008 6:01 AM CET

Report

Q3

Oct 29, 2008 7:21 AM CET

Report

Q4

Feb 18, 2009 7:03 AM CET

Report

2007

Annual report 2007

Apr 2, 2008 10:06 AM CET

Annual report 2007

Interim reports 2007

Q1

Apr 27, 2007 6:51 AM CET

Report

Q2

Jul 20, 2007 6:11 AM CET

Report

Q3

Oct 25, 2007 6:41 AM CET

Report

Q4

Feb 20, 2008 7:00 AM CET

Report

2006

Annual report 2006

Mar 22, 2007 3:32 PM CET

Annual report 2006

Interim reports 2006

Q1

Apr 28, 2006 8:55 AM CET

Report

Q2

Aug 3, 2006 6:46 AM CET

Report

Q3

Oct 25, 2006 6:33 AM CET

Report

Q4

Feb 14, 2007 7:51 AM CET

Report

2005

Annual report 2005

Mar 28, 2006 10:01 AM CET

Annual report 2005

Interim reports 2005

Q1

Apr 20, 2005 9:07 AM CET

Report

Q2

Jul 21, 2005 6:47 AM CET

Report

Q3

Oct 25, 2005 9:22 AM CET

Report

Q4

Feb 15, 2006 9:44 AM CET

Report

2004

Annual report 2004

Apr 4, 2005 8:08 AM CET

Annual report 2004

Interim reports 2004

Q1

Apr 26, 2004 8:58 AM CET

Report

Q2

Jul 21, 2004 9:20 AM CET

Report

Q3

Oct 26, 2004 9:10 AM CET

Report

Q4

Feb 11, 2005 11:09 AM CET

Report

2003

Annual report 2003

Apr 19, 2004 9:26 AM CET

Annual report 2003

Interim reports 2003

Q1

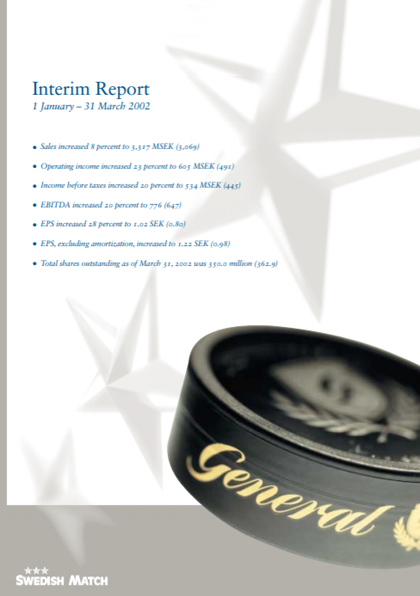

Apr 25, 2003 9:46 AM CET

Report

Q2

Jul 23, 2003 10:01 AM CET

Report

Q3

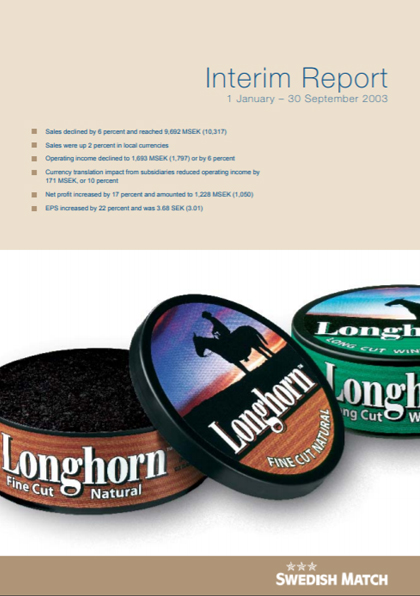

Oct 23, 2003 9:18 AM CET

Report

Q4

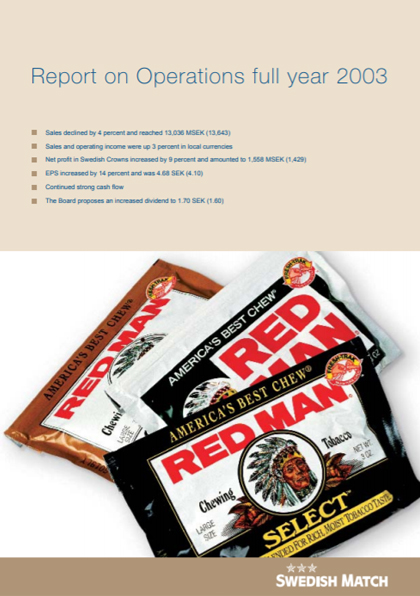

Feb 11, 2004 10:40 AM CET

Report

2002

Annual report 2002

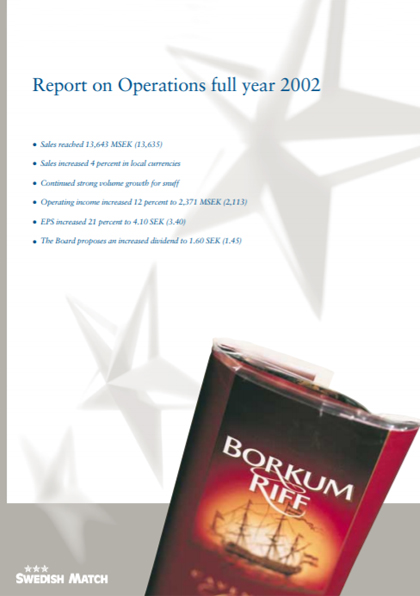

Feb 11, 2003 3:06 PM CET

Annual report 2002

Interim reports 2002

Q1

Apr 23, 2002 9:30 AM CET

Report

Q2

Jul 24, 2002 9:54 AM CET

Report

Q3

Oct 24, 2002 9:25 AM CET

Report

Q4

Feb 11, 2003 10:48 AM CET

Report

2001

Annual report 2001

Apr 12, 2002 2:06 PM CET

Annual report 2001

Interim reports 2001

Q1

Apr 24, 2001 2:35 PM CET

Report

Q2

Jul 24, 2001 2:30 PM CET

Report

Q3

Oct 23, 2001 9:28 AM CET

Report

Q4

Feb 12, 2002 11:18 AM CET

Report

2000

Annual report 2000

Feb 8, 2001 3:06 PM CET

Annual report 2000

Interim reports 2000

Q1

Apr 27, 2000 2:38 PM CET

Report

Q2

Jul 25, 2000 2:38 PM CET

Report

Q3

Oct 26, 2000 2:39 PM CET

Report

Q4

Feb 8, 2001 2:40 PM CET

Report

1999

Annual report 1999

Apr 17, 2000 10:06 AM CET

Annual report 1999

Interim reports 1999

Q1

Apr 26, 1999 2:41 PM CET

Report

Q2

Jul 27, 1999 3:06 PM CET

Report

Q3

Oct 29, 1999 2:25 PM CET

Report

Q4

Feb 9, 2000 3:40 PM CET

Report

1998

Annual report 1998

Feb 12, 1999 3:06 PM CET

Annual report 1998

Interim reports 1998

Q1

Apr 29, 1998 11:00 AM CET

Report

Q2

Aug 10, 1998 2:44 PM CET

Report

Q3

Oct 23, 1998 2:45 PM CET

Report

Q4

Feb 12, 1999 3:46 PM CET

Report

1997

Annual report 1997

Feb 24, 1998 11:06 AM CET

Annual report 1997

Interim reports 1997

Q1

May 6, 1997 2:46 PM CET

Report

Q2

Aug 12, 1997 2:47 PM CET

Report

Q3

Nov 6, 1997 3:48 PM CET

Report

Q4

Feb 24, 1998 12:15 PM CET

Report

1996

Annual report 1996

Mar 3, 1997 3:06 PM CET

Annual report 1996